Worried About Debt? You Are Not Alone!

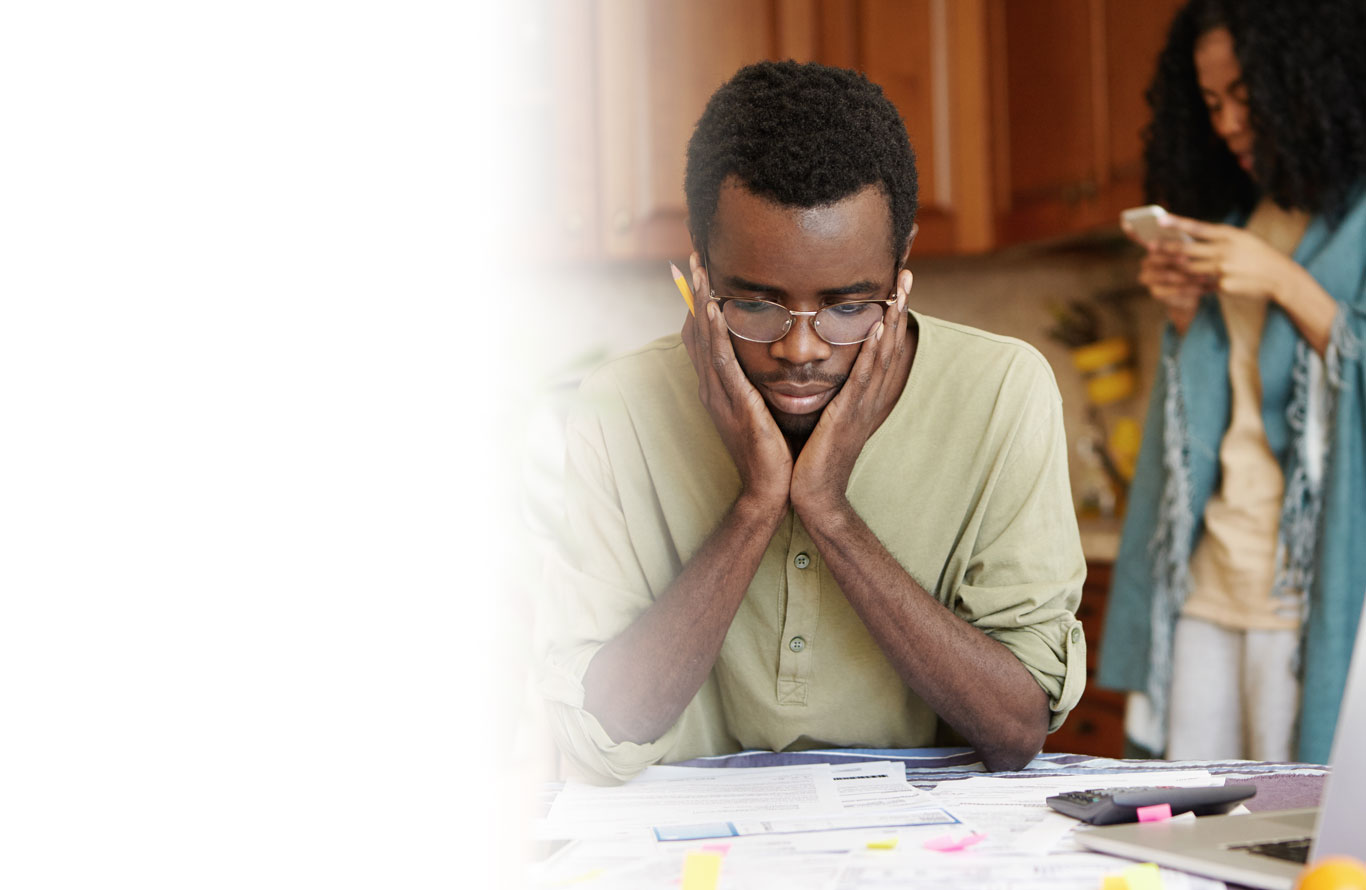

If you are lying awake at night wondering ‘How do I resolve my debt’, you are not alone. After a period during the pandemic when Canadians actually increased their savings, the house of cards seems to be crashing down around our ears. Inflation is at its highest level in forty years and this is painfully apparent in areas like groceries and rent. A host of other consumer goods are soaring in price as well.

It is also true that we live in a society where the accumulation of debt seems to get easier and easier. We are bombarded with messages urging us to consume. And, during the pandemic, Canadians shifted a good portion of their shopping to the internet – so what was once a daytime pursuit became a 24/7 one.

One group in particular has had a hard time coping with debt - the generation of students graduating now with hefty student loans. Education is increasingly expensive and entry-level salaries have not kept up. An entire cohort is taking on debt at a much earlier age.

What are the Solutions to Debt?

Debt Consolidation is a process by which your various debts are merged into a single loan. The amount of what you owe doesn’t change, but your ability to manage it does.

Having just one loan means that you are paying one fixed interest rate for a defined period of time – a much simpler setup than having a number of loans at different rates and for different terms.

With this comes ‘certainty’. It’s very clear how much you owe. You know when your payments must be made. The interest rate on the consolidated loan is not susceptible, for example, to the variance in credit card rates, which can rise and fall. There is no more confusion. And by paying just one monthly payment, you immediately achieve a much greater ease of budgeting.

If you have a good credit score and have been paying off your debts, you may be able to lock your consolidation debt loan at a lower rate than you were paying on your previous multiple loans. (This is not a sure thing, however. Much depends on your credit rating.)

As you pay down your consolidated debt, you will be boosting your credit rating over time. This is in direct contrast to the more drastic option of declaring bankruptcy, which will annihilate your chances of a good credit rating going forward.

Is There a Catch?

Debt Consolidation has a lot of positives. Simplicity, economy, clarity are among them, as well as the possibility of a better credit rating and a lower interest rate. However, the loan payments are not flexible. Unlike with credit cards, there is no ‘minimum payment’ option. Also, there are fees to set up the Consolidation Loan, as it is bringing together a number of creditors.

But if you are sinking under a large amount of debt owed to different creditors, it definitely is worth considering. If ‘Resolve my debt’ is your goal, Debt Consolidation can help you reach it.